Uniswap, the decentralized exchange (DEX) giant, has formally initiated three pivotal governance proposals aimed at activating protocol fees across a broad spectrum of its operations, encompassing various chains and different iterations of its highly influential platform. This strategic move, if approved by the community, signifies a significant shift in Uniswap’s economic model, redirecting a portion of transaction fees to the protocol’s treasury and, crucially, into the existing UNI token burn mechanism. The proposals have immediately ignited a spirited debate within the decentralized finance (DeFi) community, particularly among liquidity providers (LPs) who currently receive the lion’s share of trading fees.

The Genesis of the Fee Switch: Understanding Uniswap’s Governance and Fee Mechanics

At its core, Uniswap operates as a decentralized autonomous organization (DAO), where key decisions, such as changes to its fee structure, are determined through governance proposals voted on by holders of its native UNI token. For years, Uniswap’s design has largely prioritized liquidity providers, funneling nearly all swap fees directly to them as an incentive to supply capital and facilitate trading. This model has been instrumental in Uniswap’s meteoric rise, establishing it as the world’s leading DEX by volume.

A protocol fee, in the context of Uniswap, represents a percentage of the total swap fees that is diverted from liquidity providers and allocated to the Uniswap protocol itself. While the technical capability for a "fee switch" has long existed within Uniswap’s smart contracts, governance proposals to activate it have historically faced strong opposition, primarily from LPs concerned about reduced returns and potential liquidity drain. The current proposals mark a renewed and more expansive effort to activate this mechanism, signaling a potential maturation of Uniswap’s business strategy.

The funds collected through these protocol fees are intended to be channeled into the existing UNI burn mechanism. Token burning is a deflationary tactic where a certain amount of tokens are permanently removed from circulation. For UNI holders, this mechanism is designed to increase the scarcity and, theoretically, the value of their tokens over time, by reducing the total supply. This connection between protocol revenue and token burn is central to the current proposals’ appeal to UNI holders.

Unpacking the Proposals: Scope and Reach Across the DeFi Landscape

The current set of governance proposals outlines a comprehensive activation strategy, targeting both older and newer versions of the Uniswap protocol across a multitude of blockchain networks.

The first proposal specifically targets Uniswap V2 and V3 deployments on the newly launched Robinhood chain. The Robinhood Layer-2 (L2) network, which debuted earlier this month, has rapidly gained traction, attracting a host of decentralized applications, including a significant presence from Uniswap. In a testament to its burgeoning activity, Uniswap’s operations on the Robinhood chain remarkably surpassed $1 billion in trading volume within approximately ten days of its launch. This rapid adoption on a nascent L2 underscores the strategic importance of Robinhood Chain for Uniswap and suggests a significant potential revenue stream for the protocol if fees are activated there.

The second, and perhaps most expansive, proposal seeks to activate fees on Uniswap V4 across a broad array of prominent blockchain networks. These include Ethereum, the foundational blockchain for DeFi; leading L2 solutions like Base, Arbitrum, and Optimism; the aforementioned Robinhood chain; the BNB Chain; and Polygon. This multi-chain, multi-L2 approach highlights Uniswap’s ambition to capture value across the entire decentralized ecosystem, acknowledging the increasingly fragmented and interconnected nature of blockchain finance.

Adding to the scope, Hayden Adams, the CEO of Uniswap Labs, indicated that a third fee proposal for the remaining V4 chains not covered in the second proposal would be submitted in due course. This phased approach suggests a deliberate strategy to gradually implement the fee switch across Uniswap’s entire operational footprint, maximizing its potential impact on protocol revenue and the UNI burn mechanism.

A Strategic Shift: Hayden Adams on UNI Burn and Value Accrual

Hayden Adams articulated the strategic rationale behind these proposals, emphasizing the direct link between the new protocol fees and the UNI token’s value proposition. "Both direct all new protocol fees into the existing UNI burn mechanism," Adams stated. He further projected, "Based on current volumes, especially Robinhood, we expect the impact on UNI burn to be substantial."

This statement is critical for UNI token holders. Historically, a common criticism leveled against UNI was its lack of direct value accrual for holders, beyond governance rights. While LPs earned trading fees, the protocol itself generated minimal revenue that directly benefited UNI holders. By funneling protocol fees into a burn mechanism, Uniswap aims to create a more compelling economic model for its token, aligning the protocol’s success more directly with the value of UNI. The anticipated "substantial" impact on UNI burn, particularly driven by the impressive volumes on the Robinhood chain, suggests a potential acceleration of UNI’s deflationary trajectory.

The DeFi Debate: Mixed Reactions from Liquidity Providers

Unsurprisingly, these proposals have elicited mixed reactions across the DeFi community, particularly from the liquidity providers who stand to see a reduction in their earnings. For clarity, fees in a DEX like Uniswap are paid by users for each swap. Traditionally, these fees are predominantly directed to LPs as compensation for providing the capital that enables these swaps. Protocol revenue, on the other hand, is a percentage of these swap fees that, after a governance vote, is directed to the project itself, partly for purposes like the UNI burn.

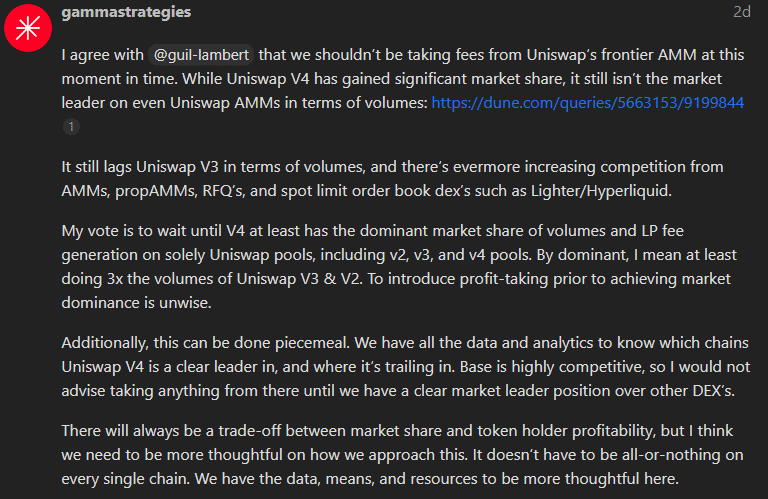

The direct implication of activating protocol fees is a reduction in the fees collected by LPs. This fundamental shift was met with immediate opposition from some LP providers. Gamma Strategies, a prominent liquidity management platform, voiced strong concerns regarding the V4 fee proposals, arguing that such a move would directly impact their "lifeline" – the revenue they derive from providing liquidity.

Gamma Strategies articulated a robust argument against the V4 fee activation, contending that Uniswap V4 is not yet sufficiently competitive to withstand a reduction in LP incentives. They highlighted that "It (V4) still lags Uniswap V3 in terms of volumes, and there’s evermore increasing competition from AMMs, propAMMs, RFQ’s, and spot limit order book DEX’s such as Lighter/Hyperliquid." This argument posits that imposing protocol fees on a version that is still striving for market dominance could hamper its growth and drive liquidity away to rival platforms that offer more attractive returns for LPs. The concern is that by making liquidity provision less profitable, Uniswap V4 might struggle to attract and retain the necessary capital to compete effectively against a rapidly evolving landscape of decentralized trading venues.

This perspective underscores a classic dilemma in decentralized finance: balancing the need for protocol sustainability and value accrual for token holders with the imperative to maintain competitive incentives for liquidity providers, who are the lifeblood of any DEX.

Historical Context: The Imbalance of Value Distribution

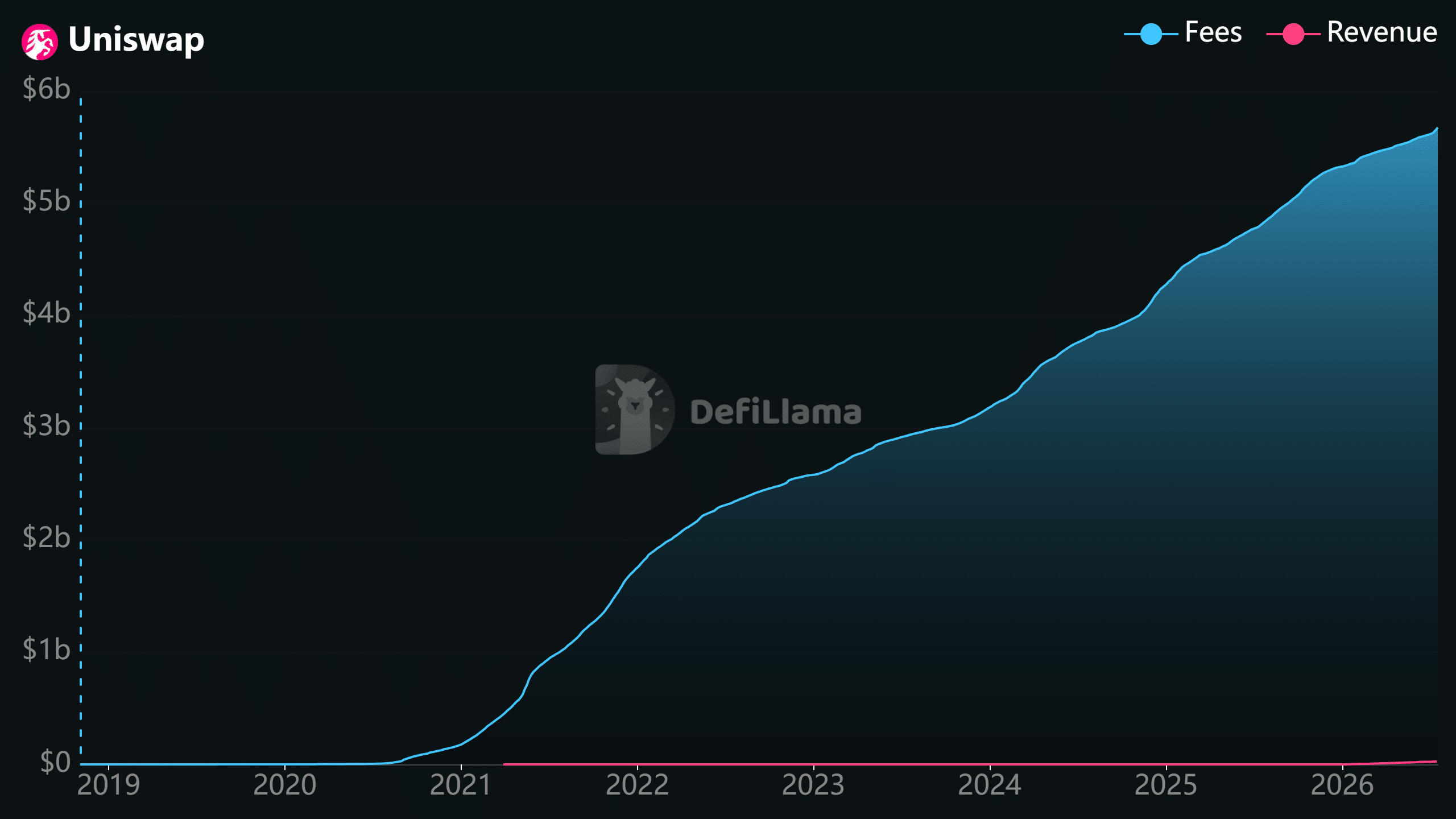

To fully appreciate the significance of these fee proposals, it’s essential to examine the historical distribution of value within the Uniswap ecosystem. Since its inception in 2018, Uniswap’s liquidity providers have collectively earned a staggering cumulative total of over $5 billion in fees. This immense sum reflects the sheer volume and activity facilitated by the platform, demonstrating the critical role LPs play.

In stark contrast, the Uniswap protocol itself has accumulated a mere $25 million in cumulative revenue over the same period. This vast disparity highlights the current model’s heavy emphasis on LP incentives, often at the expense of direct protocol value accrual. While this model fostered explosive growth and market dominance, it also raised questions about the long-term sustainability and intrinsic value of the UNI token, which primarily functioned as a governance token without a direct claim on protocol earnings.

The current proposals are a direct response to this imbalance. If approved and implemented judiciously, ensuring a delicate balance with market competition, increased protocol revenue would indeed translate into higher UNI burn rates, as projected by Hayden Adams. This shift could redefine UNI from primarily a governance token to one with a more robust economic foundation, directly benefiting its holders through a deflationary mechanism.

The Mechanism of Value: How Protocol Fees Drive UNI Burn

The proposed fee activation mechanism is designed to directly bolster the UNI token’s deflationary economics. As protocol fees are collected, they are then used to acquire UNI tokens from the open market, which are subsequently "burned," meaning they are permanently removed from circulation. This process effectively creates buying pressure for UNI and reduces its overall supply, which, under normal market conditions, can lead to an appreciation in the token’s value.

Currently, Uniswap has already burned a substantial 107.49 million UNI tokens. The recent surge in activity, particularly on the Robinhood chain, has already shown a preview of the potential impact. In the past week alone, the UNI burn rate surged threefold, jumping from an estimated $51,000 to over $160,000. This pre-existing momentum, combined with the activation of protocol fees, could significantly accelerate the rate at which UNI tokens are removed from circulation, reinforcing the token’s scarcity.

Market Dynamics: UNI’s Recent Performance and Future Outlook

The anticipation surrounding the Robinhood Layer-2 integration and the ensuing governance proposals has already manifested in Uniswap’s [UNI] price action. Traders front-ran the news, leading to a notable rally in July, where UNI’s price surged by approximately 41%, climbing from $2.70 to $3.80. This bullish momentum reflects the market’s positive reception to developments that enhance UNI’s value proposition.

However, this initial bullish strength has shown signs of easing, with the price stalling below its 200-day Moving Average (MA), a key technical indicator often used to gauge long-term trends. This technical resistance suggests that while optimism exists, the market is also exercising caution. Should the momentum from the Robinhood chain stabilize without further catalysts, UNI’s price could enter a sideways trading range, potentially holding above $3.50, or even experience a slight retracement towards the $3.00 mark.

The immediate future price trajectory of UNI will likely be dictated by two primary factors: sustained or renewed momentum from the Robinhood chain, indicating continued strong adoption and trading volumes, and the successful passage and implementation of the fee proposals, which would solidify the enhanced UNI burn mechanism. A positive outcome on both fronts could provide the necessary impetus for UNI to break above its current resistance levels and extend its rally.

Broader Implications for the DeFi Landscape

The outcome of Uniswap’s fee proposals carries significant implications that extend far beyond the protocol itself, potentially shaping the future of decentralized exchanges and the broader DeFi ecosystem.

For UNI Holders, the activation of protocol fees represents a crucial step towards making UNI a more economically robust asset. It shifts the token from primarily a governance tool to one with a direct value accrual mechanism, potentially attracting more long-term investors and enhancing its utility beyond voting. This move could inspire other major DeFi protocols to explore similar models, further integrating tokenomics with protocol revenue.

For Liquidity Providers (LPs), the impact is more nuanced. While their revenue share will directly decrease, the long-term sustainability and growth of a robust Uniswap protocol could indirectly benefit them by fostering a healthier and more active ecosystem. However, a poorly calibrated fee switch could indeed lead to liquidity migration to competing platforms, especially if those competitors offer more attractive LP incentives or innovative features. The challenge for Uniswap will be to find a "sweet spot" that generates sufficient protocol revenue without unduly penalizing LPs.

For the Uniswap Protocol itself, this is a strategic play to monetize its dominant market position. Increased protocol revenue can be reinvested into development, security audits, ecosystem grants, and further innovation, ensuring Uniswap remains at the forefront of DEX technology. It also strengthens the protocol’s treasury, providing greater financial resilience.

For the Competitive Landscape, Uniswap’s move could set a precedent. Other DEXs, many of whom already implement protocol fees, might adjust their strategies in response. Those without fees might consider implementing them, while those with existing fees might re-evaluate their percentages to remain competitive. This could lead to a broader industry trend of DEXs focusing more on sustainable revenue generation models, rather than solely relying on inflationary token incentives or solely benefiting LPs. The competition cited by Gamma Strategies, including various forms of AMMs and order book DEXs, will undoubtedly scrutinize Uniswap’s move and potentially adapt their own offerings to capitalize on any perceived vulnerabilities.

In essence, Uniswap’s governance proposals are not merely about adjusting fee percentages; they represent a fundamental re-evaluation of value distribution within a leading DeFi protocol. The outcome will be closely watched as the decentralized finance space continues to mature and seeks sustainable models for growth and innovation. The coming weeks and months will reveal whether this bold step solidifies Uniswap’s long-term viability and enhances UNI’s value, or if it inadvertently opens the door for competitors to capture market share. The delicate balance between protocol health and LP incentives remains the central tension in this unfolding narrative.

{kind=link}