Asset manager Ark Invest has openly challenged the assertions made by venture firm a16z (Andreessen Horowitz) regarding the integration of decentralized finance (DeFi) into traditional finance (TradFi), calling a16z’s perspective "overly bearish and simplistic." The crux of the disagreement centers on whether TradFi genuinely seeks the decentralized ethos of DeFi or merely the underlying blockchain technology for efficiency gains within its existing frameworks. This pivotal debate highlights a fundamental divergence in vision for the future of finance, with profound implications for blockchain development, regulatory landscapes, and market structure.

The a16z Thesis: Efficiency Over Ethos in TradFi Adoption

a16z, a prominent venture capital firm with significant investments in the crypto space, has posited that the narrative of TradFi and DeFi converging into a seamless, decentralized future is largely a "comforting story" that is "mostly wrong." According to their analysis, traditional financial institutions are not driven by an embrace of decentralization but rather by a pragmatic pursuit of cost reduction and operational efficiency. Their argument, succinctly put, is: "Where TradFi can use a blockchain to make its existing business better, it will. Not because it has embraced decentralization, but because it’s a compelling COGS (Cost of Goods Sold) story."

This perspective suggests that TradFi’s adoption is selective, cherry-picking viable innovations from the broader blockchain and DeFi ecosystem and integrating them into controlled, often permissioned, environments. The goal, from a16z’s viewpoint, is to optimize current business models rather than fundamentally reshape them around decentralized principles. They argue that this approach allows traditional players to leverage blockchain’s benefits—such as immutability, transparency within a defined network, and automated processes—while maintaining regulatory compliance, control over participants, and minimizing perceived risks associated with fully permissionless systems.

To substantiate their claims, a16z cited several key initiatives within the traditional financial sector. One prominent example is Circle’s push for Arc Chain, an institutional-grade stablecoin platform designed to facilitate large-scale, regulated payments. Arc Chain aims to provide a controlled environment where financial institutions can transact with USDC, offering features tailored for compliance, privacy, and speed within a permissioned setting. This initiative is seen as a prime illustration of TradFi favoring a blockchain solution that fits its stringent requirements for oversight and governance, rather than a truly open and permissionless DeFi protocol.

Another example highlighted by a16z is Canton Network, a burgeoning ecosystem focused on advancing privacy for institutional players dealing with tokenization. Canton is designed to enable various financial applications, from asset management to lending, on a network that prioritizes data confidentiality and regulatory adherence. Its architecture typically involves permissioned access and a focus on enterprise-grade solutions, aligning perfectly with the notion that institutions seek blockchain for specific functionalities rather than an overhaul of their operational philosophy towards decentralization.

Furthermore, a16z pointed to the Society for Worldwide Interbank Financial Telecommunication (SWIFT) and its ongoing advancements in blockchain technology for tokenization and payments. SWIFT, the backbone of global interbank messaging, has been actively piloting distributed ledger technology (DLT) solutions with numerous global banks. These initiatives aim to enhance cross-border payments, reduce settlement times, and improve reconciliation processes. However, SWIFT’s approach is typically to integrate DLT into its existing, highly regulated framework, ensuring compatibility with established financial norms and maintaining a centralized control layer. The firm concluded its argument by stating, "TradFi isn’t adopting DeFi. It’s selectively adopting parts that fit its model." This implies a strategic, rather than ideological, engagement with the nascent digital asset space.

The venture firm’s argument gained further traction when observing the selective adoption of stablecoins by major payment processors and technology giants. Companies like Mastercard, Stripe, Visa, and PayPal have integrated stablecoins into their payment rails or service offerings. While this marks a significant embrace of digital assets, a16z suggests that these adoptions are driven by the practical benefits of stablecoins—such as their efficiency for cross-border transactions, lower fees compared to traditional remittances, and the ability to serve a broader, digitally native customer base—rather than a commitment to the underlying decentralized networks or the broader DeFi ecosystem. These companies often partner with issuers like Circle or Paxos, which operate within regulated frameworks, thereby maintaining a degree of control and oversight that aligns with traditional financial principles.

Ark Invest’s Rebuttal: The Inevitability of Open Access and Public Chains

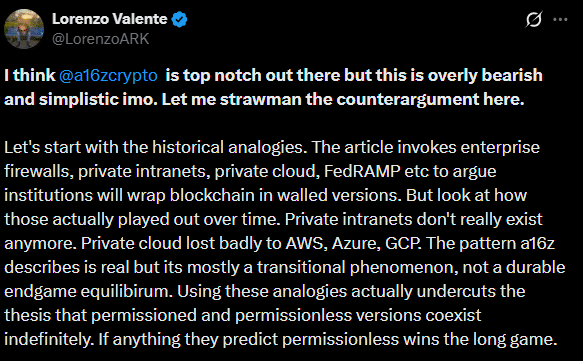

Lorenzo Valente, Director of Crypto Research at Ark Invest, offered a robust counter-argument, dismissing a16z’s stance as "overly bearish and simplistic." While acknowledging the quality of a16z Crypto’s research, Valente argued that their analysis fails to capture the full picture of TradFi’s evolving relationship with blockchain and DeFi. Ark Invest, known for its bullish long-term outlook on disruptive innovation, believes that the transformative power of decentralization and open access cannot be easily contained within permissioned, centralized environments indefinitely.

Valente highlighted several key developments that, in Ark Invest’s view, contradict a16z’s narrow interpretation. A prime example is the success of BlackRock’s BUIDL (BlackRock USD Institutional Digital Liquidity Fund), a tokenized treasury money market fund that operates on a public blockchain, specifically Ethereum. The launch of BUIDL, by the world’s largest asset manager, was a watershed moment, demonstrating a tangible commitment from a major TradFi player to leverage the transparency, liquidity, and programmability offered by a permissionless public chain for real-world asset (RWA) tokenization. This move, Valente argued, goes beyond mere efficiency gains; it signals an acceptance of the open infrastructure that underpins DeFi, allowing for broader participation and innovative composability. The ability for BUIDL to exist and thrive on Ethereum suggests that institutions are indeed finding value in the public blockchain environment, even if their initial engagement is cautious and structured.

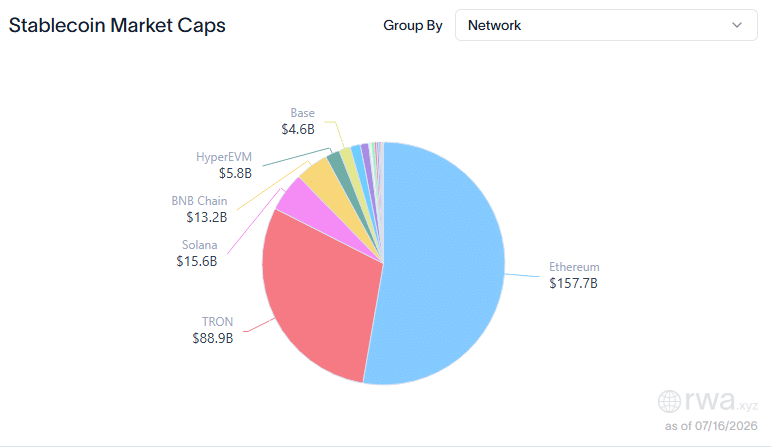

Furthermore, Valente emphasized the undeniable success and market dominance of stablecoins like USDT (Tether) and USDC (USD Coin), which primarily operate on public chains such as Ethereum and Tron. The cumulative market capitalization and daily transaction volumes of these stablecoins underscore a massive market preference for "open access." These digital dollars facilitate global remittances, peer-to-peer payments, and serve as crucial liquidity infrastructure for the broader crypto economy, often operating without the need for traditional intermediaries or cumbersome settlement processes. The sheer scale of stablecoin usage on public blockchains, accessible to anyone with an internet connection, illustrates a powerful demand for permissionless financial infrastructure that a16z’s "TradFi wants only blockchain" narrative might overlook.

Ark Invest posits that private, permissioned chains, while offering initial comfort zones for risk-averse institutions, are ultimately destined to "die in isolation unless they join permissionless public chains." This perspective aligns with the historical trajectory of network effects, where open and interoperable systems tend to outcompete closed, proprietary ones in the long run. The argument is that the true power of blockchain lies in its network effects, its ability to connect diverse participants globally without gatekeepers, and its potential for composability—where different protocols can seamlessly interact and build upon each other. Private chains, by design, limit these network effects, potentially hindering their long-term growth and utility.

This sentiment was strongly echoed by Carlos Domingo, CEO of Securitize, a leading tokenization issuer. Domingo articulated that "Private chains or pseudo ones are the intranet and private clouds of this era, a transitional step into a truly open and permissionless innovation model." This analogy suggests that while private blockchains serve a current need for institutions dipping their toes into the digital asset waters, they represent an interim phase, much like corporate intranets before the widespread adoption of the open internet. The ultimate evolution, according to this view, will inevitably lead towards a more integrated and permissionless financial landscape, where public blockchains act as the global rails for value transfer and asset ownership.

The Nuanced Reality: Data-Driven Insights and Market Dynamics

The debate between Ark Invest and a16z is not merely theoretical; it is underpinned by observable market data that presents a more complex and nuanced picture. While both firms present compelling arguments, the current landscape suggests a dynamic interplay between permissioned and permissionless systems, with different segments of the market gravitating towards distinct solutions.

In the stablecoin market, the dominance of public chains is undeniable. Data indicates that Ethereum and Tron collectively control nearly 75% of the stablecoin sector by market capitalization and transaction volume. This significant market share reflects the success of open, permissionless networks in facilitating global, real-time value transfer for both retail and institutional users. The liquidity, composability with DeFi protocols, and broad accessibility offered by these public chains have made them the preferred settlement layers for stablecoin transactions. For instance, the ability to seamlessly integrate stablecoins into decentralized exchanges, lending platforms, and other DeFi applications on Ethereum creates a powerful ecosystem that private chains struggle to replicate due to their inherent limitations on access and interoperability. The ease of sending USDC or USDT across borders, 24/7, without relying on traditional banking hours or intermediaries, highlights the practical advantages of public chain adoption in this specific domain.

However, when examining the tokenization of real-world assets (RWAs), the landscape shifts considerably, lending credence to a16z’s perspective. Corporate and permissioned chains like Canton Network and Provenance Blockchain currently command a massive 85% market share in the tokenized assets segment, particularly for institutional-grade applications. Ethereum, despite its robust DeFi ecosystem, comes in third with approximately 4% of this market. This stark difference underscores the institutional preference for environments that offer enhanced control, privacy, and regulatory compliance for complex assets such as private equity, real estate, or structured products. For many financial institutions, the ability to implement Know Your Customer (KYC) and Anti-Money Laundering (AML) checks at the protocol level, manage access permissions for specific assets, and ensure data confidentiality are paramount concerns that are more readily addressed by permissioned blockchain solutions. Provenance Blockchain, for example, is specifically designed for financial services, providing the infrastructure for regulated entities to issue, manage, and transact tokenized securities and loans with the necessary legal and compliance frameworks built-in.

The emergence of new private chains further complicates the narrative. Companies like Stripe with Tempo, and Google with the Google Cloud Universal Ledger (GCUL), are actively developing or piloting their own Layer 1 blockchain solutions. These initiatives are squarely focused on payments and tokenization, aiming to offer enterprise-grade solutions that leverage blockchain benefits while operating within controlled environments. Stripe Tempo, for instance, seeks to enhance payment efficiency for businesses, potentially integrating with existing financial infrastructure in a way that prioritizes speed, reliability, and regulatory adherence. Google Cloud Universal Ledger (GCUL) could offer similar capabilities, providing a blockchain backbone for enterprise applications that demand high throughput, robust security, and seamless integration with Google’s cloud services, all within a managed, permissioned framework. These developments validate the idea that major tech and finance players are keen to harness blockchain, but often on their own terms, in settings that provide greater governance and oversight.

Deeper Analysis: Convergence, Divergence, and Hybrid Models

The ongoing debate between Ark Invest and a16z illuminates the fundamental philosophical and practical challenges at the intersection of TradFi and DeFi. It’s not simply a question of which side is "right," but rather a reflection of the complex evolutionary path of financial technology.

TradFi’s inherent risk aversion and stringent regulatory obligations are powerful drivers for its preference for permissioned environments. The existing financial system is built on layers of trust, legal contracts, and intermediaries, all designed to mitigate systemic risk and protect consumers. Introducing fully permissionless, decentralized systems without clear regulatory frameworks presents significant challenges for compliance, liability, and operational stability. Therefore, institutions often opt for solutions that allow them to maintain control over participants, enforce compliance rules, and manage data privacy, even if it means sacrificing some degree of decentralization. This approach allows them to experiment with blockchain technology in a sandbox-like environment, gradually integrating features that prove beneficial without disrupting their core operations or incurring undue regulatory scrutiny.

Conversely, DeFi’s foundational principles are rooted in transparency, censorship resistance, and user ownership, all enabled by open, permissionless public blockchains. The ethos of DeFi champions a world where financial services are accessible to anyone, anywhere, without the need for intermediaries or centralized authorities. This vision, while revolutionary, often clashes with the established norms of traditional finance, particularly concerning identity verification, anti-money laundering, and consumer protection. However, the innovation velocity and the emergent properties of open, composable protocols on public chains are undeniable. The ability for developers to permissionlessly build new financial applications on top of existing ones fosters an ecosystem of rapid iteration and novel solutions that private, siloed chains struggle to match.

The current data suggests that the future of finance is unlikely to be a simple convergence or divergence, but rather a complex ecosystem characterized by hybrid models and interoperability. It is plausible that permissioned blockchains will continue to serve specific institutional needs, particularly for highly regulated assets or intra-organizational processes. These "intranets" of the financial world could provide the initial testing grounds and controlled environments necessary for institutions to gain confidence in DLT. However, as Carlos Domingo suggested, these private chains may eventually seek to connect with public blockchains to tap into broader liquidity, greater network effects, and enhanced interoperability.

This could manifest in several ways:

- Permissioned layers on public chains: Institutions might deploy permissioned smart contracts or operate within specific zones on public blockchains, allowing them to leverage the underlying security and decentralization while maintaining control over access and identity for their specific applications.

- Cross-chain bridges and interoperability protocols: Technologies enabling seamless communication and asset transfer between permissioned and permissionless chains could create a more integrated financial landscape. This would allow institutions to originate assets on private chains for compliance, but then move them to public chains for broader liquidity and distribution.

- Regulated DeFi: The emergence of "permissioned DeFi" or "institutional DeFi" aims to bridge this gap by building DeFi protocols that incorporate regulatory compliance (e.g., KYC/AML whitelisting) while still leveraging the benefits of public blockchains. Projects like Aave Arc are examples of this trend, offering pools accessible only to whitelisted institutions.

Implications for the Future of Finance

The debate between Ark Invest and a16z has significant implications for the long-term trajectory of the financial industry.

- Innovation Landscape: The dynamic tension between these two perspectives will continue to drive innovation. TradFi’s demand for efficient, compliant blockchain solutions will spur development in enterprise DLT, privacy-enhancing technologies, and scalable infrastructure. Concurrently, the DeFi ecosystem will continue to push the boundaries of open finance, decentralization, and composability, challenging traditional paradigms.

- Regulatory Evolution: Regulators worldwide are grappling with how to oversee this rapidly evolving space. The existence of both permissioned and permissionless systems presents a complex challenge. Regulatory frameworks may need to adapt to accommodate hybrid models, distinguishing between highly controlled institutional applications and open, public protocols. Clarity on issues like digital asset custody, stablecoin regulation, and tokenized securities will be crucial for both TradFi and DeFi adoption.

- Market Structure: The future financial market may be a multi-layered ecosystem, with public blockchains acting as global settlement layers for certain asset classes (like stablecoins) and permissioned blockchains serving as specialized infrastructure for others (like complex RWAs). The interoperability between these layers will be key to unlocking maximum value.

- User Adoption: For retail users, the debate might lead to more diverse product offerings, from highly regulated tokenized funds to fully decentralized financial services. For institutional users, it could mean greater efficiency and new investment opportunities, but within frameworks that meet their compliance needs.

In conclusion, while a16z’s argument highlights the pragmatic, efficiency-driven motivations of traditional finance’s initial engagement with blockchain, Ark Invest’s counter-narrative emphasizes the transformative, long-term potential of open access and decentralization. The current market data suggests that both sides hold elements of truth. Public chains dominate stablecoin payments due to their open nature and vast liquidity, while corporate chains maintain a significant moat in the tokenized assets segment, catering to institutional demands for control and compliance. The future of finance will likely be a complex interplay of these forces, evolving towards a hybrid ecosystem where the benefits of both permissioned efficiency and permissionless innovation are leveraged, rather than a simple victory for one vision over the other. The journey towards this integrated future is still unfolding, marked by continuous innovation, regulatory adaptation, and a vibrant, ongoing debate among the industry’s leading minds.